This post is adapted from ARtillery Intelligence’s report, Spatial Computing: 2019 Lessons, 2020 Outlook. It includes some of its data and takeaways. More can be previewed here and subscribe for the full report.

At this stage of spatial computing’s lifecycle, it’s becoming clear that patience is a virtue. After passing through the boom and bust cycle of 2016 and 2017, the last two years were more about measured optimism in the face of the sobering realities of industry shakeout and retraction.

At the precipice of 2020, that leaves the question of where we are now? Optimism is still present but AR and VR players continue to be tested as high-flying prospects like ODG, Meta and Daqri dissolve. These events are resetting expectations on the timing and scale of revenue outcomes.

But there are also confidence signals. 2019 was more of a “table-setting” year for our spatial future and there’s momentum building. Brand spending on sponsored mobile AR lenses is a bright spot, as is Apple AR glasses rumors. And Oculus Quest is a beacon of hope on the VR side.

To synthesize where we are and where we’re going, our research arm ARtillery Intelligence has published its annual year-end recap and year-forward outlook. This includes five predictions, listed below. Following our deep dive on #1, #2, #3, and #4, we’ll now drill down on #5: VR’s 2020 fate.

1. Apple Glasses Don’t Arrive in 2020

2. AR Wins With “Training Wheels”

3. Advertising Keeps the AR Revenue Crown

4. Industrial AR’s Inflection is Still One Year Away

5. VR Has an Evolutionary (not revolutionary) 2020

Prediction 5: VR’s Evolutionary 2020

VR will continue to make important strides and hit milestones in 2020. But it will be a long, slow road, rather than the revolutionary cultural takeover that proponents expected in the circa-2016 hype cycle. The catalyst will continue to be Facebook’s VR investments to accelerate adoption.

This includes continued momentum for Oculus Quest and additional Facebook investments like content libraries and supporting tech (e.g. Oculus Link, and hand tracking). These moves will attract more users to Quest — and VR by association — given a more compelling overall package.

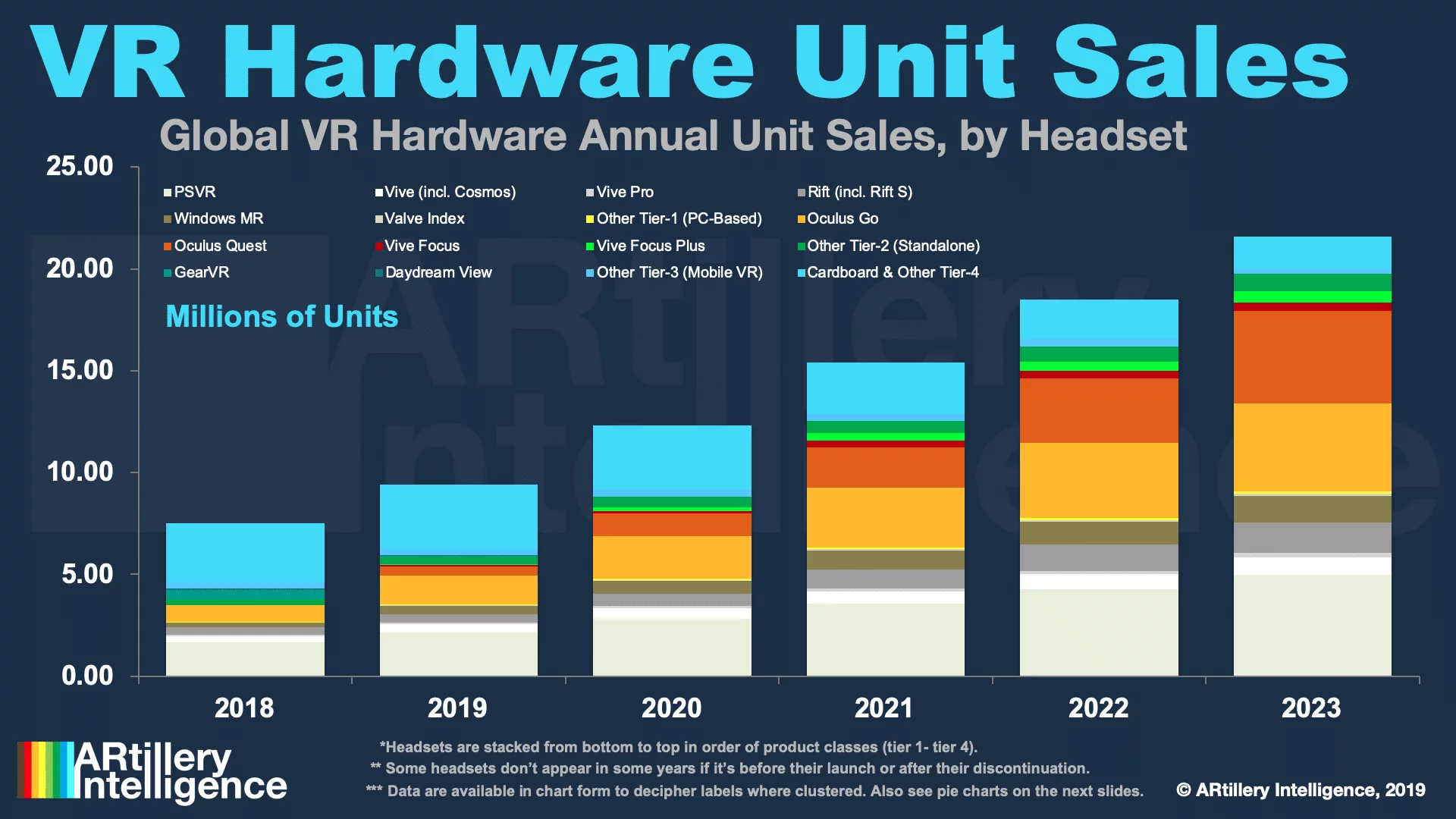

The market will also continue to diverge, with Oculus’ market share growing in the product classes where it competes. That includes tier-1 tethered (Rift S), tier-2 standalone (Quest) and lean-back 3DoF VR (Go). Its loss-leader pricing will take market share from margin-dependent competitors.

The exception will be hardware that has specialized use cases – such as Vive PRO and Varjo’s focus on enterprise-grade specs. But those market-share wins will be smaller in quantity than Oculus’s consumer-based VR growth in 2020. Oculus will pull ahead in the aggregate.

Oculus will also continue to invest in content, including buying rather than building, as it did with Beat Games. This represents a divergence from its previous strategy with Oculus Story Studio. This means exit potential for AR startups and will stimulate innovation and seed investments.

These factors will result in more robust VR content libraries, more users, and greater software spending per user (ARPU). This virtuous cycle will take a while to ratchet up, but is the process that Oculus will continue to accelerate through its platform-driven long-term investment approach.

Boiling it Down

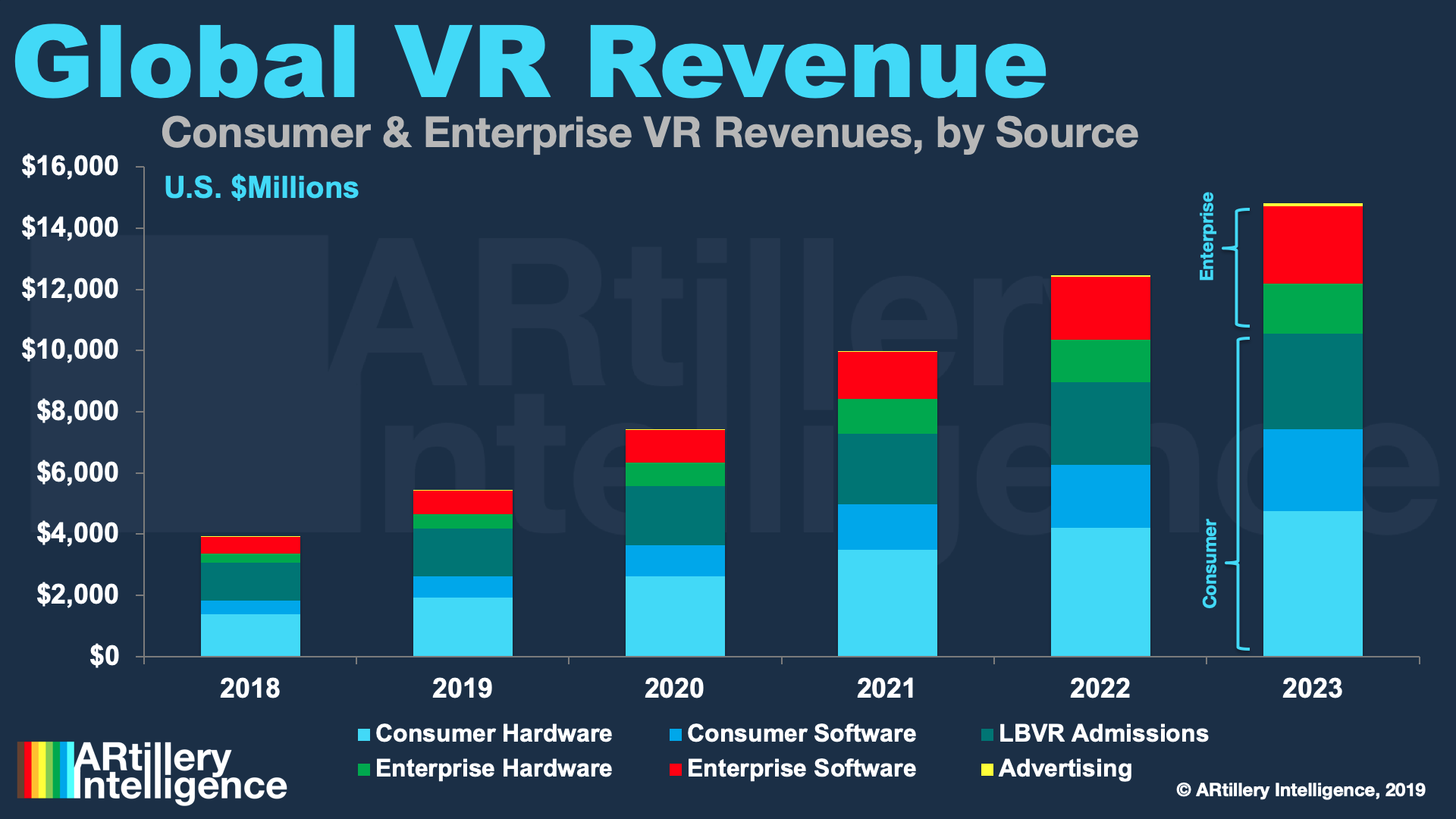

As for a concrete and quantifiable prediction, ARtillery Intelligence projects VR to grow from $5.4 billion in 2019 to $7.4 billion in 2020 and $14.8 billion by 2023. That’s led by hardware for the entire forecast period, but software will gain share as it builds on a growing installed base.

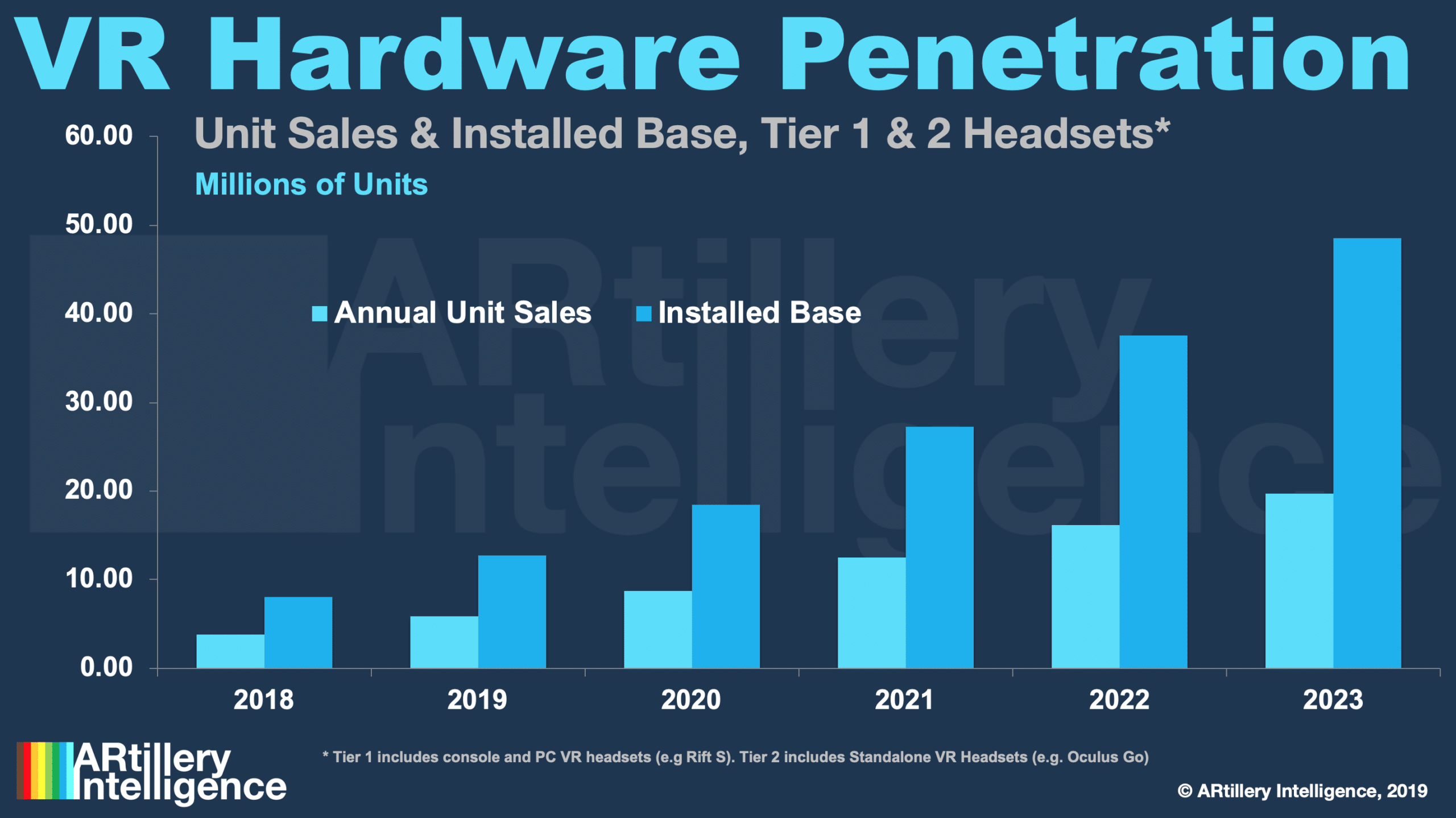

Hardware will specifically grow from $1.9 billion last year to $2.6 billion in 2020, on pace for $4.8 billion by 2023. This correlates to tier-1 (tethered) and tier-2 (standalone) annual unit sales of 8.79 million in 2020, and a cumulative installed base of 12.73 million in-market headsets by year-end.

The most notable headset — Oculus Quest per the above factors — was specifically projected to reach revenue of $178 million in 2019, growing to $399 million in 2020 and $1.58 billion by 2023. That correlates to 470,000 unit sales in 2019, 1.11 million in 2020, and 4.54 million by 2023.

Of course outer-year projections are speculative, though based on market signals ARtillery tracks closely. It will be a moving target that requires course correction as market factors continue to unfold. We’ll track all of the above into 2020 and report back. Meanwhile, see the full report here.

For deeper XR data and intelligence, join ARtillery PRO and subscribe to the free AR Insider Weekly newsletter.

Disclosure: AR Insider has no financial stake in the companies mentioned in this post, nor received payment for its production. Disclosure and ethics policy can be seen here.