AR shouldn’t be viewed as one monolithic industry but rather a series of subsectors, each at different stages and following different market dynamics. That includes mobile AR, headworn AR, and subsegments like advertising, commerce, gaming and enterprise productivity.

To maintain focus and to adequately examine the depth of each of these nuanced areas, our research arm ARtillery Intelligence subdivides its market forecasts. For example, its recent mobile AR forecast quantified smartphone-based AR such as advertising and location-based gaming.

With that forecast under its belt, the firm recently turned attention to AR glasses and their many moving parts. The result is its report, Headworn AR Global Revenue Forecast, 2019 – 2024. This is also the topic of the latest episode of ARtillery Briefs, with takeaways and video below.

Common Pattern

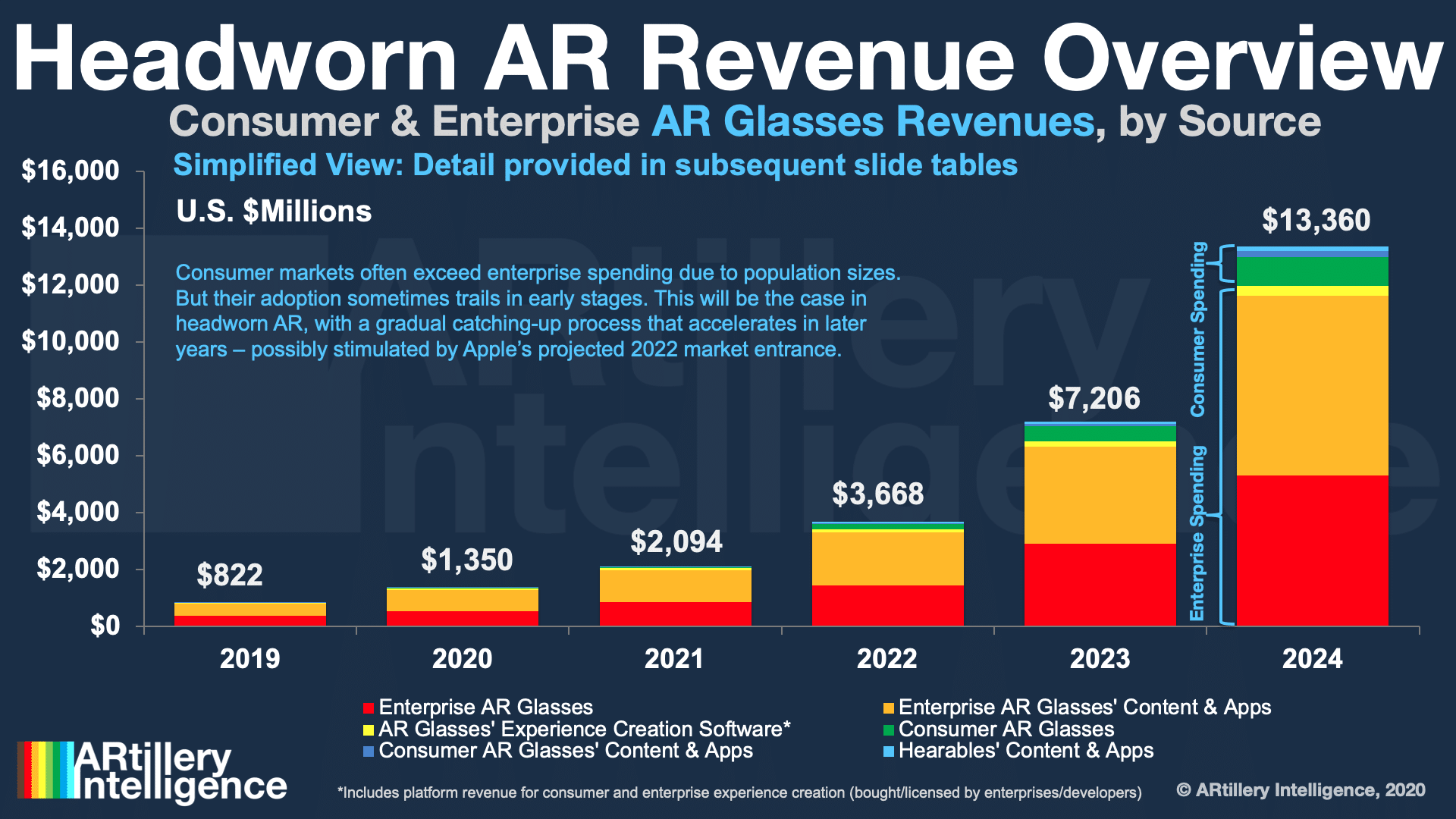

So what did the forecast uncover? Global headworn AR revenue is projected to grow from $822 million last year to $13.4 billion by 2024. That sum consists of consumer and enterprise spending — the latter holding a majority share. It’s further subdivided by hardware and software.

Hardware leads in early years, but software will outpace it over time. This happens as a larger installed base accumulates, and as software average revenue per user (ARPU) grows. This is a common pattern for emerging technology, which we saw in the smartphone’s early days.

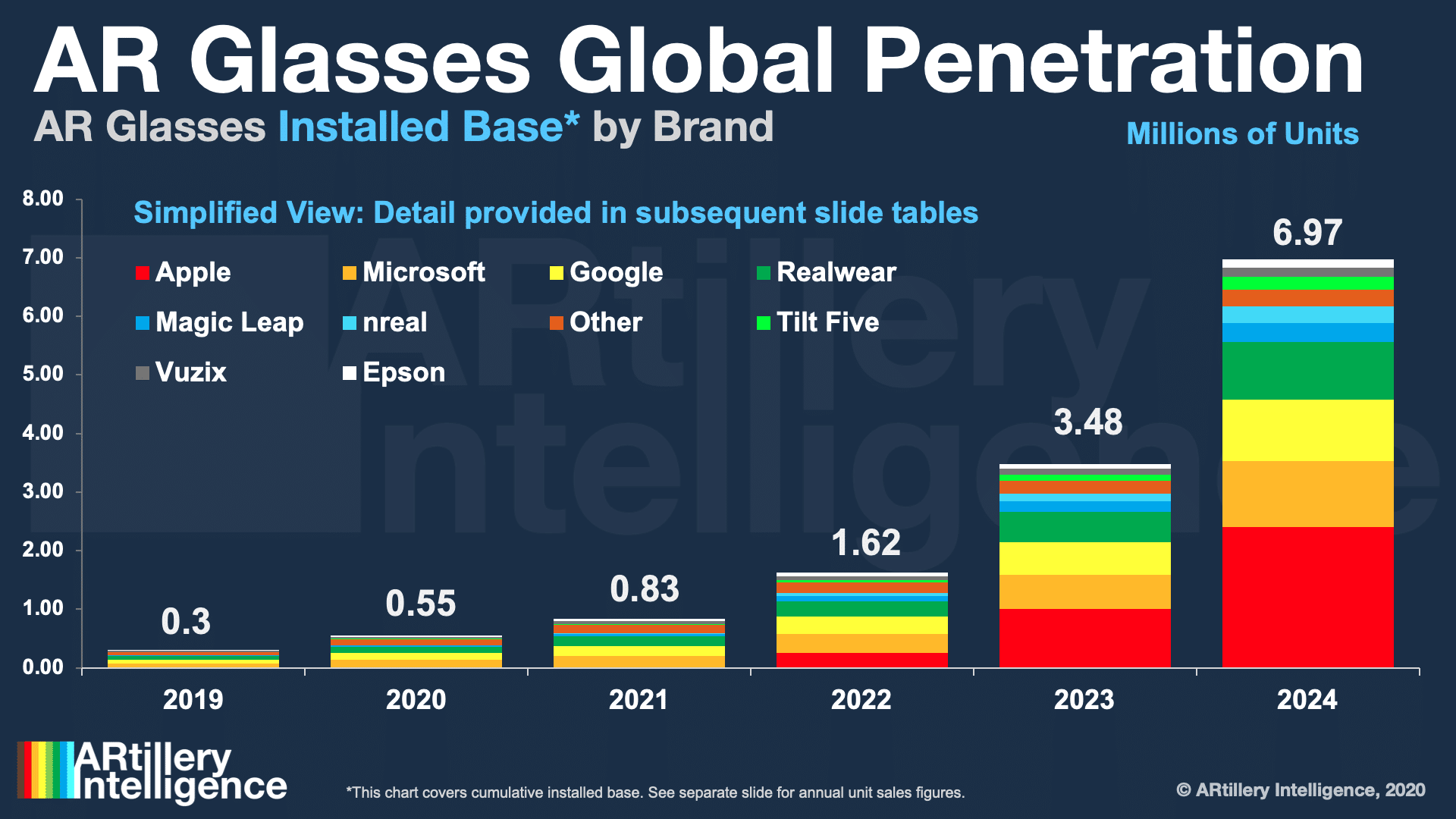

Quantifying that hardware base, AR headsets unit sales are projected to grow from 170,000 last year to 3.9 million in 2024 — an installed base of 7 million units at that time. This includes enterprise and consumer hardware, the former dominating in early years by about 14 to 1.

Enterprise’s spending share is primarily driven by a strong business case for AR-guided productivity in areas like assembly, maintenance, and field service. This total also includes the U.S. Army’s multi-year contract with Microsoft to deploy Hololens 2 for logistics and combat.

But it’s also worth noting that consumer spending will catch up in later years. Consumer markets are generally larger, though enterprise spending can lead in early stages of emerging tech sectors. Consumer spending will also grow from improving hardware and cultural acclimation.

Wild Card

Another factor that could stimulate a consumer AR spending shift is Apple. Its smart glasses are projected to hit the market in 2022, which could create a classic Apple “halo effect.” This is when Apple raises all boats by acclimating consumers and stimulating market demand.

“Apple Glass” is projected to sell 259,000 units in its first year, 758,000 in 2023 and 1.4 million in 2024 (see chart below). In terms of revenue, the consumer AR glasses market will consist of AR glasses themselves, as well as the software-based experiences that run on those glasses.

Notably, that could contrast mobile AR consumer software spending which is dominated by in-app purchases, mostly from Pokemon Go. AR glasses software could instead include a mix of premium apps (similar to how content is sold in VR) and recurring content subscriptions.

AR glasses use cases could also be defined by Apple in terms of the software marketplaces it creates, just like it did in mobile. With ARkit, it’s already laid the groundwork and anchored its position as a central hub for AR experiences that run on (and drive demand for) its AR hardware.

Some use cases are already evident such as Apple’s Project Gobi, which involves QR codes that unlock promotions at retail partners. Its V1 AR glasses could otherwise prioritize style over graphical intensity and feature “lite AR” such as notifications, filters and vision correction.

The Covid Impact

All of the above just scratches the surface and you can see more in the full report and in the ARtillery Briefs episode below. But one note in closing is that Covid-era dynamics will impact headworn AR through factors like supply-chain impediments and recessionary spending.

Those detriments could be partially offset by Covid factors that boost AR. Those include enterprise remote assistance, whose guided support aligns with social distancing requirements. Either way, Covid-impediments impact the near term, with the sector back on track by the end of 2021.

From there, it’s a matter of gradually unseating smartphones as the primary AR modality. Though smart glasses are a longer-term play for market penetration, they’re eventually AR’s fully-actualized modality. So it’s a matter of gradual evolutionary steps towards that end.